Understanding the marginal cost formula is crucial for businesses aiming to optimize production processes, manage budgets effectively, and make informed decisions regarding pricing strategies. This formula reveals the additional cost incurred by producing one more unit of a product, thereby providing deep insights into production economics.

Why Marginal Cost Matters

The marginal cost formula is vital for businesses, as it serves as a key indicator of the financial implications of increasing production. By pinpointing the cost of producing an additional unit, firms can determine the optimal output level that maximizes profit and minimizes waste. Companies can use this knowledge to adjust pricing, predict revenues, and streamline operations.

Key Insights

- Primary insight with practical relevance: Marginal cost analysis helps businesses determine optimal production levels, thus balancing cost and revenue efficiently.

- Technical consideration with clear application: Calculating marginal cost involves understanding variable costs per unit and fixed costs which do not change with production volume.

- Actionable recommendation: Regularly revisiting marginal cost calculations enables continuous improvements in production efficiency and cost management.

Breakdown of the Marginal Cost Formula

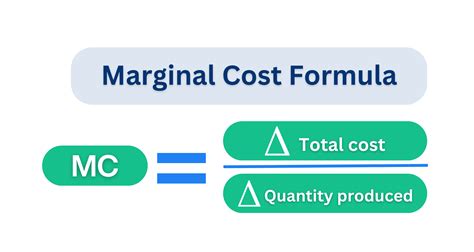

The marginal cost (MC) formula is mathematically represented as follows: MC = ΔC / ΔQ, where ΔC denotes the change in total cost and ΔQ signifies the change in quantity produced. This simple yet powerful formula helps businesses understand how the cost alters with each additional unit produced. Let’s consider a practical example to clarify this concept. Suppose a manufacturing company produces bicycles. If the total cost rises by 100 when production increases from 100 to 101 bicycles, the marginal cost for the 101st bicycle is 100. This direct insight allows managers to decide if producing additional units is economically feasible.

Applications in Business Strategy

Marginal cost is not just a theoretical construct but a practical tool that can significantly influence business strategy. For instance, a company aiming to expand its market share might initially produce extra units at a marginal cost lower than the market price to undercut competitors. This strategic maneuver could lead to long-term profitability even if initial margins are thin. Conversely, firms must avoid the pitfall of producing too many units where the marginal cost exceeds the selling price, as this results in a loss on each additional unit. Efficient use of the marginal cost formula ensures that a business stays agile and responsive to market dynamics while maintaining a robust bottom line.

How does marginal cost differ from average cost?

While marginal cost focuses on the cost of producing one additional unit, average cost considers the total cost per unit produced on average. Average cost is calculated by dividing total costs by the quantity produced. Understanding both metrics is crucial for comprehensive cost management.

Can marginal cost be negative?

In rare cases, marginal cost can be negative if the revenue generated from selling an additional unit is greater than the variable costs associated with its production. This situation typically occurs in industries with high fixed costs, allowing for cost savings when utilizing underutilized capacity.

In conclusion, mastery of the marginal cost formula equips businesses with essential knowledge for operational and strategic decision-making. The insights derived from this formula can guide effective resource allocation, pricing strategies, and ultimately contribute to sustainable growth.