Mastering the Marginal Cost Equation: A Key to Business Success

Understanding the marginal cost equation can be a game-changer for your business. It is crucial in determining how additional costs are incurred when producing more units of a product. This guide will provide you with a clear, step-by-step roadmap to mastering this concept, complete with practical examples and actionable advice to ensure your business thrives.

Understanding Marginal Cost: The Problem and Solution

Marginal cost is the additional cost incurred by producing one more unit of a product. Understanding this concept is pivotal for efficient business operations, especially for those looking to maximize profitability. Often, businesses struggle with accurately calculating marginal cost, leading to poor decision-making in production levels and pricing strategies. The problem is exacerbated when businesses fail to adapt this knowledge to real-world scenarios, which results in unnecessary financial strain and missed opportunities. By mastering the marginal cost equation, you can make informed decisions that enhance efficiency, optimize production, and ultimately drive business success.

Our goal is to break down the marginal cost equation into a user-friendly guide that offers practical solutions to real-world business problems. With this knowledge, you’ll be better positioned to manage your costs, set competitive prices, and scale your operations effectively.

Quick Reference

- Immediate action item: Calculate your current marginal cost by identifying fixed and variable costs, and assess how it changes as you produce more units.

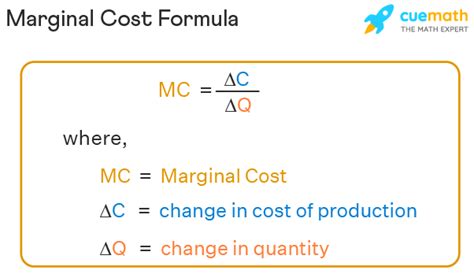

- Essential tip: Use the marginal cost equation: MC = ΔC / ΔQ, where MC is the marginal cost, ΔC is the change in total cost, and ΔQ is the change in quantity produced.

- Common mistake to avoid: Confusing marginal cost with average cost; ensure you understand that marginal cost only looks at the cost of producing one more unit.

Breaking Down the Marginal Cost Equation: Step-by-Step Guidance

To start with the basics, we’ll dissect the marginal cost equation. By understanding each component and seeing how they interact, you’ll gain the insight needed to apply this knowledge effectively.

What is Marginal Cost?

Marginal cost (MC) represents the change in total cost when one additional unit of a product is produced. It includes only the variable costs that change with the level of production.

For instance, if your fixed costs (rent, salaries) remain constant and your only variable cost (materials, labor for one more unit) is 5, then the marginal cost of producing that unit is 5.

Formulating the Marginal Cost Equation

The marginal cost equation is straightforward: MC = ΔC / ΔQ

Where:

- ΔC (change in total cost): This is the difference in total cost between producing N units and (N-1) units.

- ΔQ (change in quantity): This is the difference in the number of units produced, specifically one unit in our context.

Here’s an example: Suppose your total cost changes from 1,000 to 1,100 when you increase production from 100 to 110 units. The ΔC is 100 and the ΔQ is 10 units. Therefore, MC = 100 / 10 = $10.

Identifying Fixed and Variable Costs

Understanding the distinction between fixed and variable costs is crucial. Fixed costs don’t change with the level of production, whereas variable costs do.

- Fixed costs might include rent, insurance, and salaries.

- Variable costs could encompass raw materials, packaging, and commission on sales.

To find your marginal cost accurately, you must isolate the variable costs. For instance, if producing an additional widget costs 2 in raw materials but the rent remains at 1,000 regardless of how many widgets you produce, the marginal cost is solely the $2 spent on raw materials.

Analyzing Marginal Cost Over Different Production Levels

As you increase production, the marginal cost may fluctuate due to economies or diseconomies of scale.

- Initially, increasing production might lead to economies of scale, where the marginal cost decreases as you spread fixed costs over more units.

- At some point, marginal costs might begin to rise due to diseconomies of scale, such as increased inefficiencies or higher costs for raw materials.

For example, if your first 100 units have a marginal cost of 10 each, but your next batch sees this cost increase to 15 due to material scarcity or labor inefficiencies, your marginal cost has risen.

How to Implement Marginal Cost Calculation in Your Business

Here’s a step-by-step guide to implement marginal cost calculations in your business:

- Identify your variable costs: List out all the variable costs associated with each unit of product. Ensure this includes all incremental costs like raw materials, labor, and shipping.

- Determine your fixed costs: Note down all the fixed costs that remain constant regardless of production volume.

- Calculate total cost: Add up all fixed and variable costs to determine your total cost at various production levels.

- Compute marginal cost: Use the formula MC = ΔC / ΔQ to determine the additional cost for producing each additional unit.

Advanced Applications: Leveraging Marginal Cost for Strategic Decisions

Beyond simple calculations, leveraging the marginal cost equation can greatly enhance your strategic planning.

Pricing Strategy

Understanding marginal cost helps in setting prices. To avoid losing money on each sale, your price should cover both fixed and variable costs and ideally include a profit margin. For example, if your marginal cost is $10 per unit and your fixed costs per unit are low, you can set your selling price higher to ensure profitability.

Production Optimization

Use marginal cost data to decide on optimal production levels. Knowing when marginal costs start to rise can alert you to inefficiencies or approaching diseconomies of scale. You can then adjust production to maintain profitability and efficiency.

Decision Making

When evaluating new projects or expanding production lines, marginal cost analysis is vital. It helps in predicting how additional production will affect overall costs, ensuring that the benefits outweigh the costs.

How do I determine if my current production level is profitable?

To determine if your current production level is profitable, you should compare the marginal cost to your selling price. Your selling price must cover the marginal cost and ideally, include enough profit margin to cover fixed costs and yield a profit. Here’s how to do it:

- Calculate the marginal cost using the formula MC = ΔC / ΔQ.

- Determine your selling price per unit.

- Check if your selling price exceeds the marginal cost. If it does, your current production level is profitable.

- To cover fixed costs and make a profit, ensure your selling price is significantly higher than your marginal cost.

For example, if your marginal cost is $15 and your selling price is $30 per unit, you are profitable. However, if your marginal cost rises to $25 and your selling price remains at $30, you need to reconsider to avoid losses.

Conclusion: Harnessing the Power of Marginal Cost

Mastering the marginal cost equation is fundamental for business success. By understanding and applying this concept, you can make more informed decisions about pricing, production, and expansion. Remember to keep a close eye on both your variable and fixed costs, and use the marginal cost equation as a guiding tool to ensure your business remains profitable and competitive.

As you grow, continually revisit your marginal cost calculations to adapt to changing market conditions and operational efficiencies. With this powerful tool in your arsenal, you’re well-equipped to navigate the complexities of business operations and drive sustainable growth.

By following this guide, you’ll not only understand the marginal cost equation but also leverage it to enhance your business’s profitability and efficiency.

This guide provides an extensive overview of