The American Opportunity Tax Credit (AOTC) offers a powerful incentive for families investing in higher education. However, many parents and students underutilize its full potential. Maximizing your AOTC can significantly reduce the amount of money needed out of pocket for college tuition and related expenses. Here, we delve into the expert strategies and practical insights to make the most of this valuable tax credit.

Understanding the AOTC

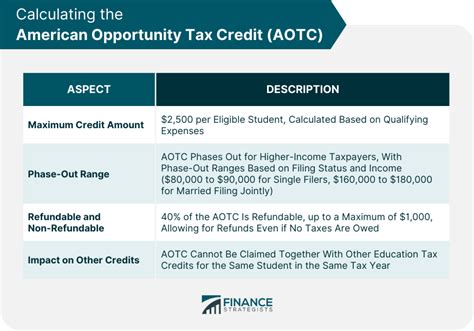

The American Opportunity Tax Credit is available for the first four years of higher education and can cover up to 100% of the first 2,000 and 25% of the next 2,000 in qualified education expenses. This means that eligible taxpayers can receive up to $2,500 per eligible student annually. With such a compelling incentive, it’s crucial to understand how to maximize this credit effectively.Key Insights

- Claim the maximum allowable credit by maximizing qualified education expenses.

- Consider funding through 529 plans or prepaid tuition plans to ensure maximum credit eligibility.

- Prioritize timing in education expenses to qualify for the highest possible credit amount in any given tax year.

Strategic Planning for Maximum AOTC Utilization

To maximize the AOTC, strategic planning is essential. Start by calculating the qualified education expenses, which include tuition, fees, books, and even certain supplies. It’s important to note that the expenses need to be for courses that meet your school’s credit hour requirement for a full-time student status. Here are some strategies to enhance your credit utilization.The first strategy involves using 529 plans or prepaid tuition plans. Contributions to these accounts are made with pre-tax dollars, and the earnings grow tax-free if used for qualified education expenses. This not only amplifies the AOTC but also benefits from compounding over time, turning the investment into a significant financial boost.

Another tactic is to prioritize the timing of educational expenses. For example, incurring expenses in the summer months or at the beginning of the academic year ensures that the costs are reported in the tax year you wish to claim the credit. Moreover, consider taking advanced or dual enrollment courses in high school. These courses may qualify as education expenses and therefore maximize the amount you can claim.

Real-Life Examples and Successful Implementation

Consider Jane, a mother of two college-bound kids. By strategically timing her contributions to their 529 plans and maximizing the annual contribution limits, she was able to secure significant tax refunds every year for four years. Additionally, she utilized the pre-tax dollars to pay for her older child’s summer courses, allowing her to claim the maximum possible credit.Another example is John, who coordinated with his local community college to enroll in dual enrollment programs that offered affordable credits. He successfully used his earned credits to fulfill college-level requirements, reducing the overall burden on his family finances and maximizing his AOTC credit.

Can I carry forward unused AOTC amounts?

No, unused AOTC amounts cannot be carried forward or refunded. It’s crucial to use it to the maximum extent in the applicable tax year.

Are there any limitations on who can claim the AOTC?

Yes, the credit is limited to the first four years of higher education and must be claimed by the taxpayer who has paid the qualified education expenses, generally the student's parents or guardian.

By implementing these strategies, you can significantly enhance your tax benefits while making a meaningful investment in your future education. The AOTC is not just a credit—it’s a financial opportunity to ease the burden of education expenses. Therefore, understanding and leveraging this credit can make a substantial difference in your overall college funding strategy.