Pristine accounting practices rely heavily on various financial statements, among which the adjusted trial balance stands out for its crucial role in financial reporting. This document is a pivotal part of the accounting cycle, ensuring the accuracy and completeness of financial data before preparing the financial statements. In this article, we will delve into the intricacies of the adjusted trial balance, offering expert perspective and practical insights to equip accountants in their daily tasks.

Key Insights

- An adjusted trial balance serves as the foundation for accurate financial statements.

- Adjusting entries address the timing differences in revenue and expenses.

- Always ensure that total debits equal total credits after making adjustments.

To comprehend the adjusted trial balance, it’s essential to grasp the process of making adjusting entries. These entries are made to account for revenues and expenses that have not yet been recorded in the accounts. For instance, if a company has earned revenue but has not yet recorded it, an adjusting entry will record this revenue in the correct accounting period. Similarly, companies often need to record prepaid expenses, such as rent or insurance, that have been paid in advance but are not yet consumed. Without these adjustments, financial statements would reflect an inaccurate picture of a company’s financial health.

Understanding Adjusting Entries

Adjusting entries are integral to the preparation of financial statements. These entries ensure that revenues and expenses are recognized in the correct periods according to the accrual accounting principles. For instance, if a company pays its annual rent in advance, it must split this payment into monthly expenses to reflect the actual usage of the rented space over time. These entries may seem trivial, but their cumulative effect is substantial. They provide a clear and accurate picture of a company’s financial performance and position, making them indispensable for decision-making and compliance with financial regulations.The Role of the Adjusted Trial Balance

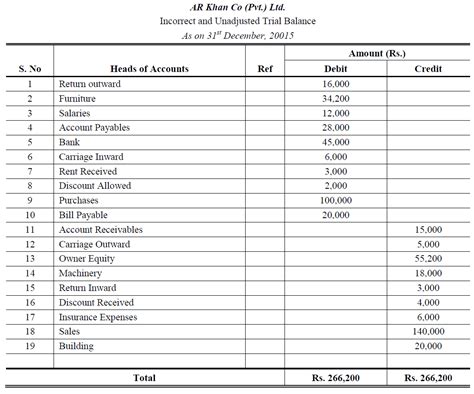

The adjusted trial balance is a critical document that lists all accounts with their adjusted balances after the accountant has made the necessary adjusting entries. This document serves to verify that the total debits equal the total credits, ensuring the fundamental accounting equation remains balanced. The adjusted trial balance is then used to prepare the financial statements, including the income statement, balance sheet, and statement of cash flows. An accountant must meticulously verify every entry to avoid discrepancies that could mislead stakeholders about the company’s financial status.An example elucidates the importance of the adjusted trial balance. Consider a company that reports revenue at the end of the month. Without an adjusted trial balance, the financial statements may reflect incomplete or inaccurate revenue data. By making the appropriate adjusting entries, the accountant ensures that all earned revenue is accounted for accurately, thus presenting a true and fair view of the company’s financial status.

What happens if the adjusted trial balance does not balance?

If the adjusted trial balance does not balance, it indicates an error in the recording of transactions, adjusting entries, or a clerical mistake. An accountant must meticulously review the trial balance, identify and correct the discrepancies, and ensure that the total debits equal the total credits before proceeding to prepare the financial statements.

How often should adjusting entries be made?

Adjusting entries should be made at the end of each accounting period, be it monthly, quarterly, or annually. This ensures that all revenues and expenses are recorded in the correct period, aligning with the accrual basis of accounting principles.

In conclusion, the adjusted trial balance is an indispensable tool in the accountant’s toolkit, providing a critical check to ensure the accuracy and completeness of financial statements. By understanding the importance of adjusting entries and ensuring that the adjusted trial balance is balanced, accountants can uphold the integrity of the financial information presented to stakeholders, thereby supporting informed decision-making and regulatory compliance.